Skip to content

Skip to content

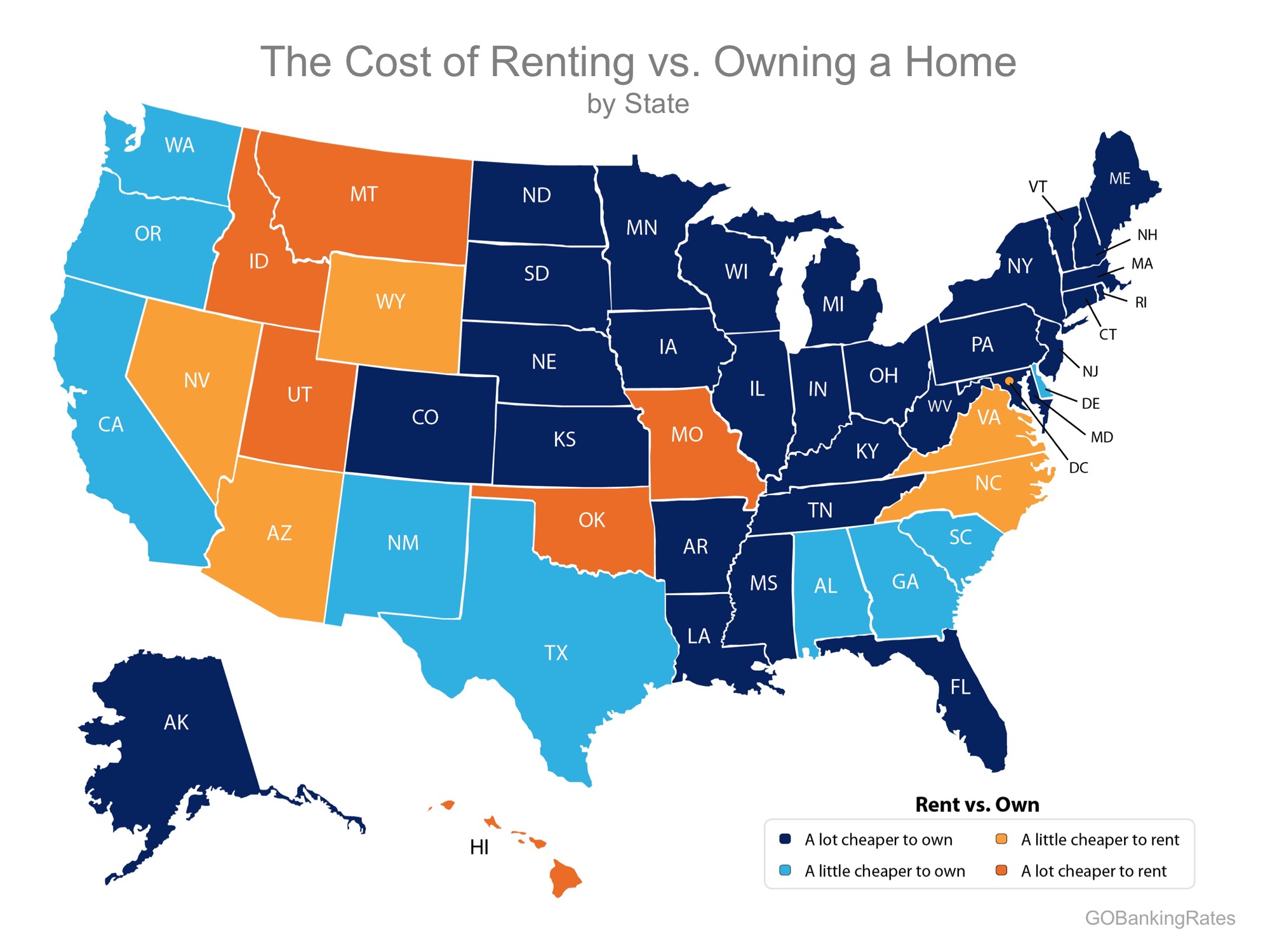

Every year at this time, many homeowners decide to wait until after the holidays to put their homes on the market for the first time, while others who already have their homes on the market decide to take them off until after the holidays.

Here are seven great reasons not to wait:

- Relocation buyers are out there. Many companies are still hiring throughout the holidays and need their employees in their new positions as soon as possible.

- Purchasers who are looking for homes during the holidays are serious buyers and are ready to buy now.

- You can restrict the showings on your home to the times you want it shown. You will remain in control.

- Homes show better when decorated for the holidays.

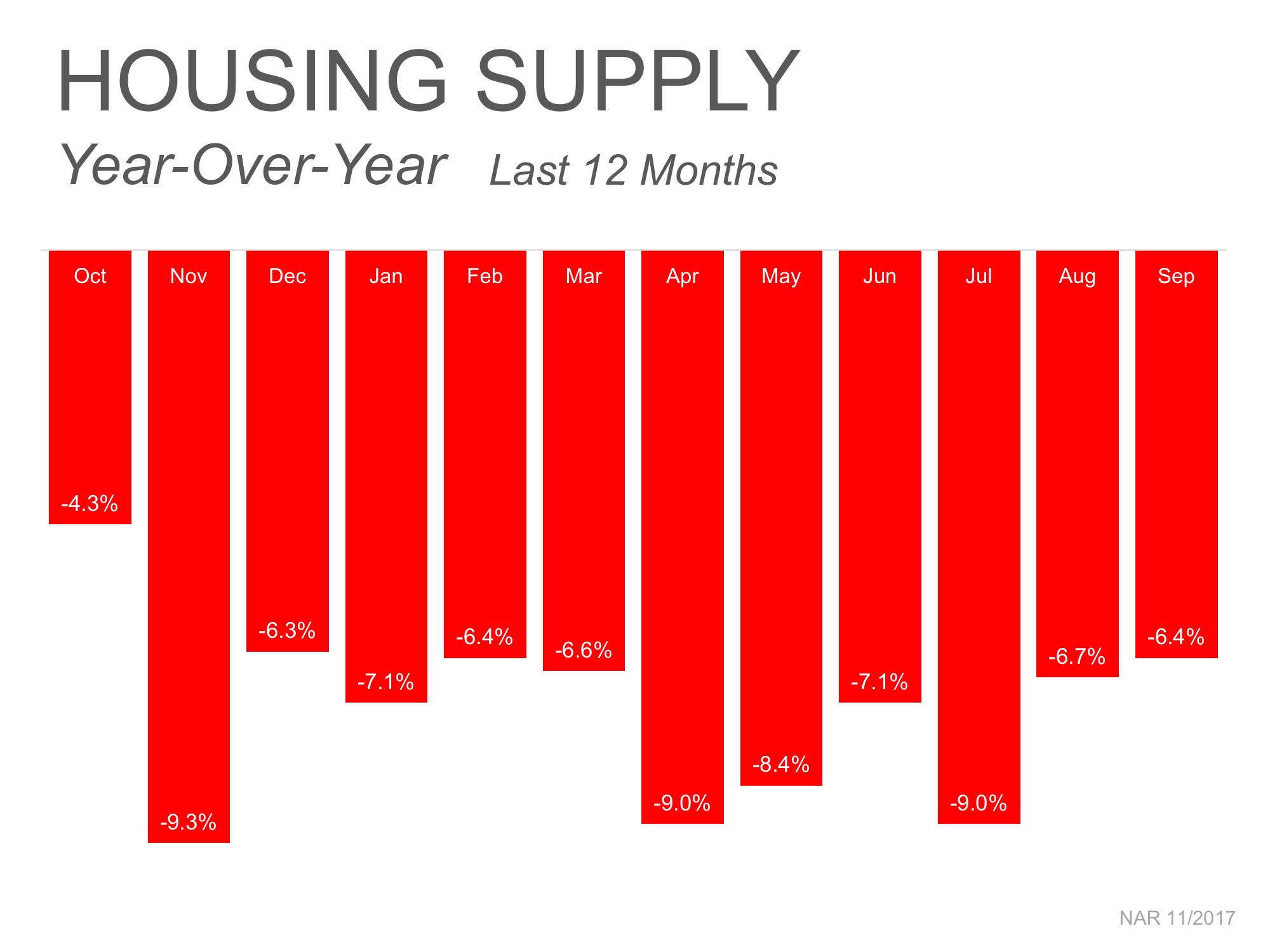

- There is less competition for you as a seller right now. Let’s take a look at listing inventory as compared to the same time last year:

- The desire to own a home doesn’t stop when the holidays come. Buyers who were unable to find their dream home during the busy spring and summer months are still searching!

- The supply of listings increases substantially after the holidays. Also, in many parts of the country, new construction will continue to surge reaching new heights in 2018, which will lessen the demand for your house.

Bottom Line

Waiting until after the holidays to sell your home probably doesn’t make sense.

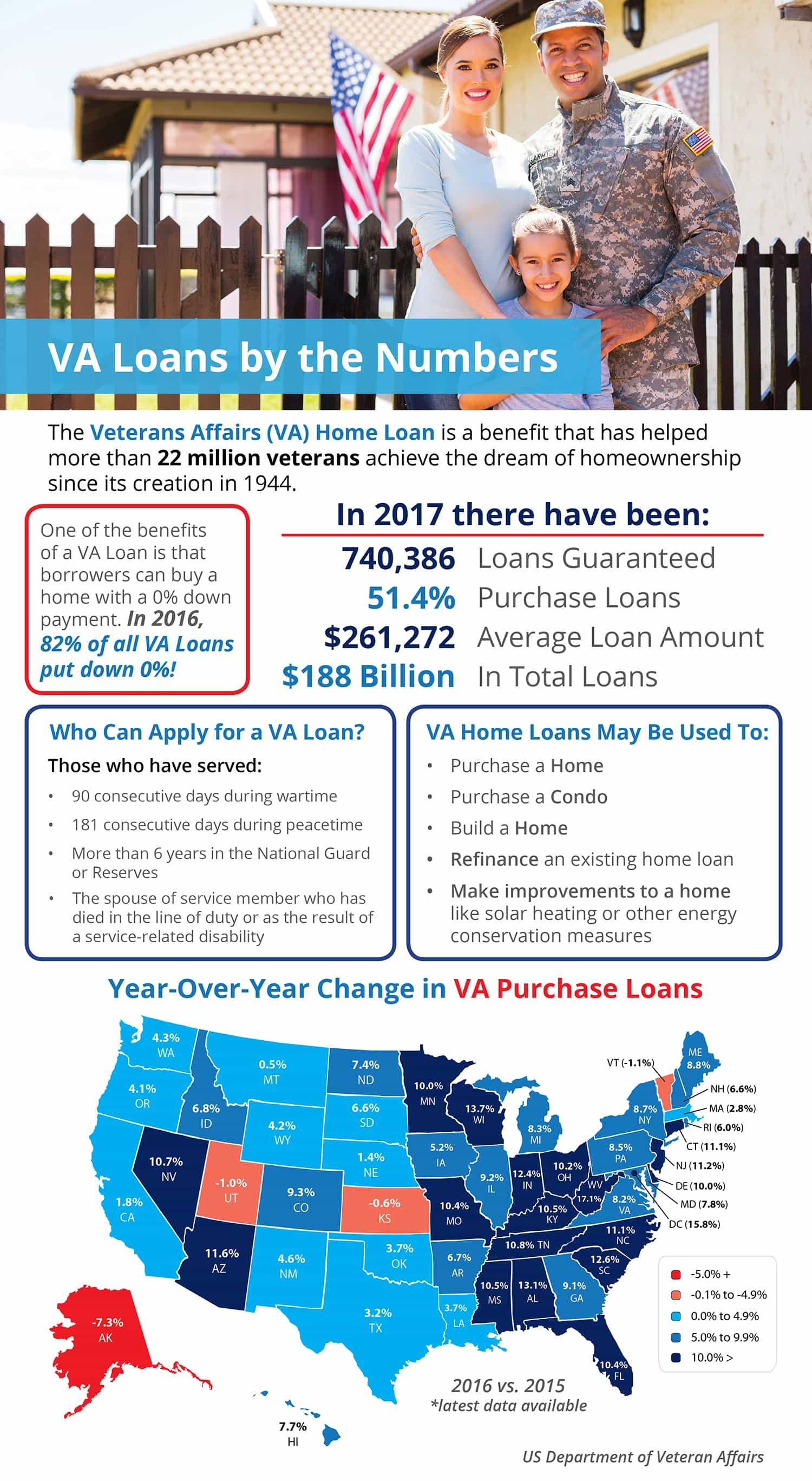

service members.

As an MRP, her training covers:

Requirements for VA financing including benefits and eligibility

Knowledge of housing options available to service members and their families

Guidance through the rent/buy/sell decision- making process as it applies to military relocation

Given her extensive training in the policies and procedures of military relocation, we are confident she can help you find housing solutions that work.

Whitney Stephens 1-801-440-7850

service members.

As an MRP, her training covers:

Requirements for VA financing including benefits and eligibility

Knowledge of housing options available to service members and their families

Guidance through the rent/buy/sell decision- making process as it applies to military relocation

Given her extensive training in the policies and procedures of military relocation, we are confident she can help you find housing solutions that work.

Whitney Stephens 1-801-440-7850

![The Difference an Hour Makes This Fall in Real Estate [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/10/25124029/The-Difference-an-Hour-Can-Make-STM.jpg)

![The Cost of Renting vs. Buying a Home [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/10/19155904/20171020-Share-STM.jpg)

![The Cost of Renting vs. Buying a Home [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/10/19155844/20170623-Rent-vs.-Buy-STM.jpg)