Multigenerational homes are coming back in a big way! In the 1950s, about 21%, or 32.2 million Americans shared a roof with their grown children or parents. According to an article by Realtor.com, “Nearly 1 in 5 Americans is now living in a multigenerational household – a household with two or more adult generations, or grandparents living with grandchildren – a level that hasn’t been seen in the U.S. since 1950.”

Another report that proves this point is the National Association of Realtors’ (NAR) 2017 Profile of Home Buyers and Sellers which states that 13% of home buyers purchased multigenerational homes last year. The top 3 reasons for purchasing this type of home were:

- To take care of aging parents (22%, up from 19% last year)

- Cost savings (17%)

- Children over the age of 18 moving back home (16%, up from 14% last year)

Valerie Sheets, Spokesperson for Lennar, points out that,

“Everyone is looking for the perfect home for any number of family situations, such as families who opt to take care of aging parents or grandparents at home, or millennials looking to live with their parents while they attend school or save for a down payment.”

For a long time, nuclear families (a couple and their dependent children) became the accepted norm, but John Graham, co-author of “Together Again: A Creative Guide to Successful Multigenerational Living,” says, “We’re getting back to the way human beings have always lived in – extended families.”

This shift can be attributed to several social changes over the decades. Growing racial and ethnic diversity in the U.S. population helps explain some of the rise in multigenerational living; “Data suggest that multigenerational living is more prevalent among Asian (28%), Hispanic (25%), and African-American (25%) families, while U.S. whites have fewer multigenerational homes (15%).”

Additionally, women are a bit more likely to live in multigenerational conditions than are their male counterparts (12% vs. 10%, respectively). Last but not least, basic economics.

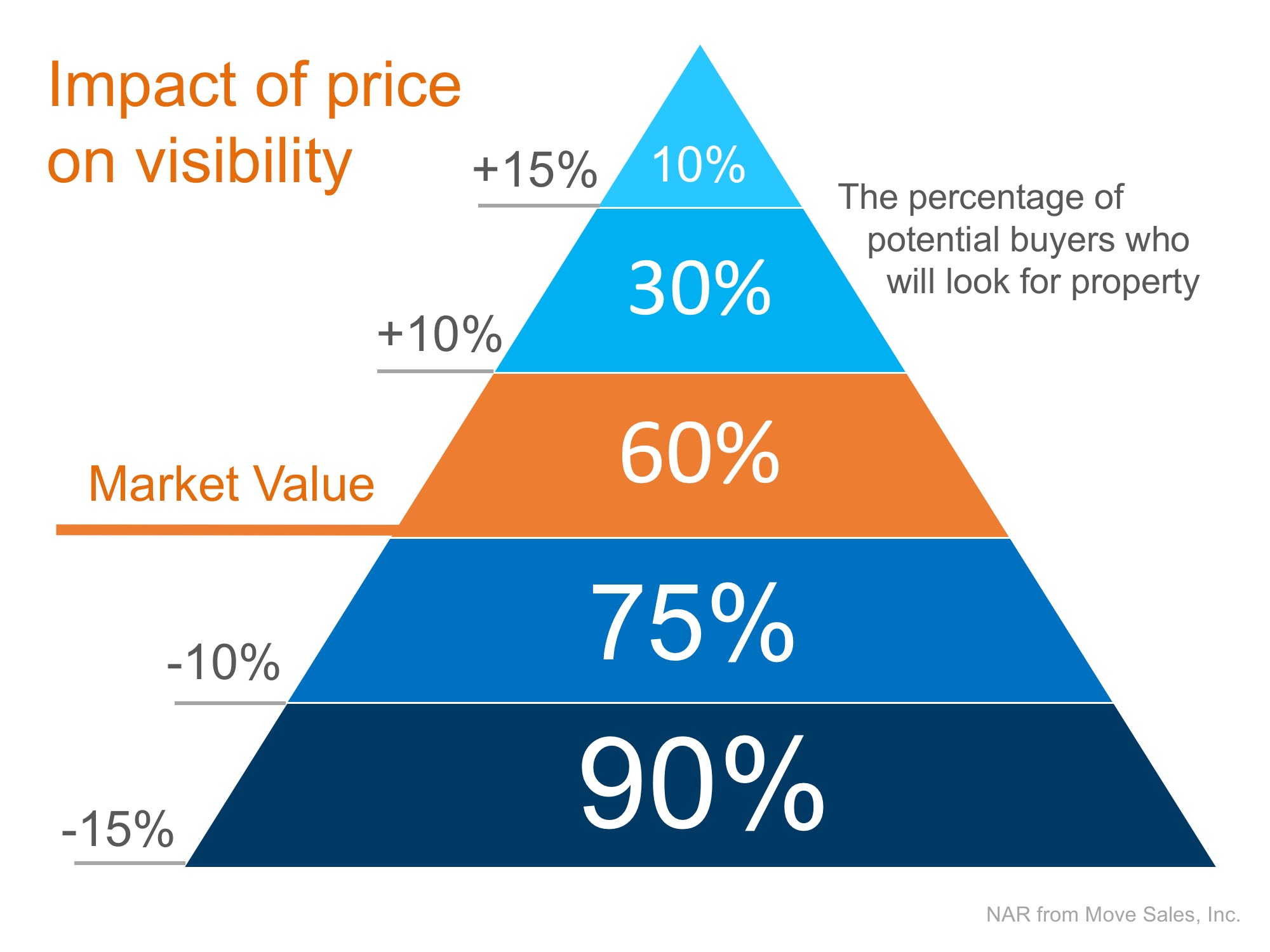

Valerie Sheets brings to light the fact that home prices have been skyrocketing in recent years. She says that, “As home prices increase, more families tend to opt for living together.”

Bottom Line

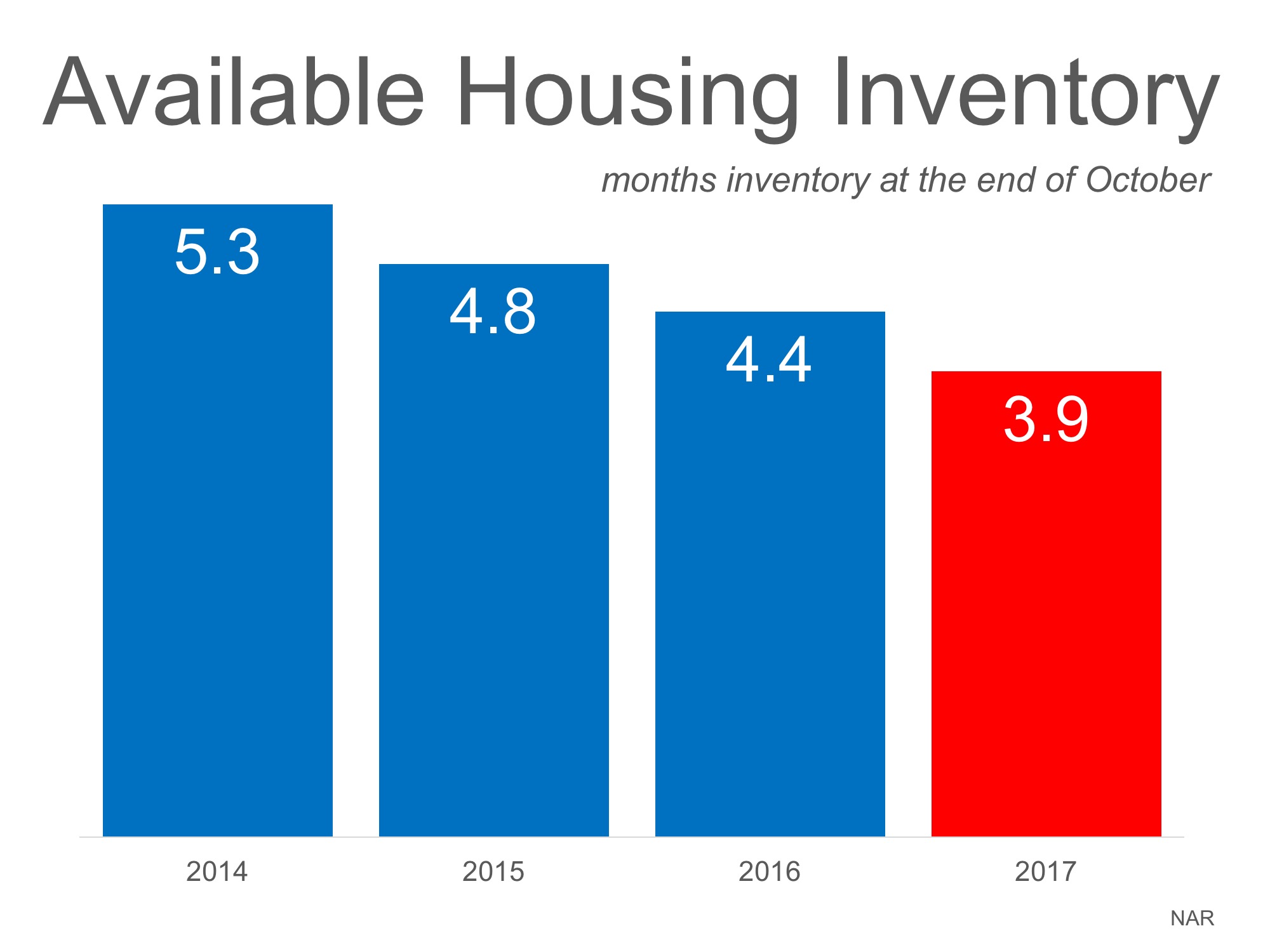

Multigenerational households are making a comeback. While it is a shift from the more common nuclear home, these households might be the answer that many families are looking for as home prices continue to rise in response to a lack of housing inventory.

Skip to content

Skip to content

![Home Prices Up 6.54% Across the Country! [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2017/12/08140910/FHFA-Home-Prices-STM.jpg)

![Should I Buy a Home Now? Or Wait Until Next Year? [INFOGRAPHIC]| Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/09/28125015/20170929-Share-STM.jpg)

![Should I Buy a Home Now? Or Wait Until Next Year? [INFOGRAPHIC]| Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/09/28124955/Cost-of-Waiting-STM.jpg)

![Lack of Existing Home Inventory Slows Sales Heading into Fall [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/09/20125536/20170922-EHS-Report-STM.jpg)